Meeting Date: March 18-19, 2025

Federal Open Market Committee (FOMC) Meeting Results

FOMC meeting highlights:

- The Fed left rates unchanged, so the current Fed Funds rate range remains at 4.25% – 4.50%. This meeting’s vote was not unanimous.

- The FOMC, which began to shrink its securities portfolio on June 1, 2022, announced it will continue to reduce its holdings of Treasury securities and agency debt and agency mortgage-backed securities. But, beginning in April of 2025, the Committee will slow the pace of decline for its securities holdings by reducing the monthly redemption cap on Treasury securities from $25 billion to $5 billion. The Committee will maintain the monthly redemption cap on agency debt and agency mortgage-backed securities at $35 billion.

- Voting against this action was Christopher J. Waller, who supported no change for the federal funds target range but preferred to continue the current pace of decline in securities holdings.

- The Committee emphasized that it is strongly committed to returning inflation to its 2% objective.

Economic highlights:

- “Recent indicators suggest that economic activity has continued to expand at a solid pace.”

- “The unemployment rate has stabilized at a low level in recent months, and labor market conditions remain solid.”

- “Inflation remains somewhat elevated.”

- “The Committee seeks to achieve maximum employment and inflation at the rate of 2% over the longer run.”

- “Uncertainty around the economic outlook has increased. The Committee is attentive to the risks to both sides of its dual mandate.”

Announcements:

- “In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 4-1/4% to 4-1/2%.”

- “In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook and the balance of risks.”

- “The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. But, beginning in April of 2025, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $25 billion to $5 billion. The Committee will maintain the monthly redemption cap on agency debt and agency mortgage-backed securities at $35 billion.”

- “In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook.”

- “The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals.”

- “The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.”

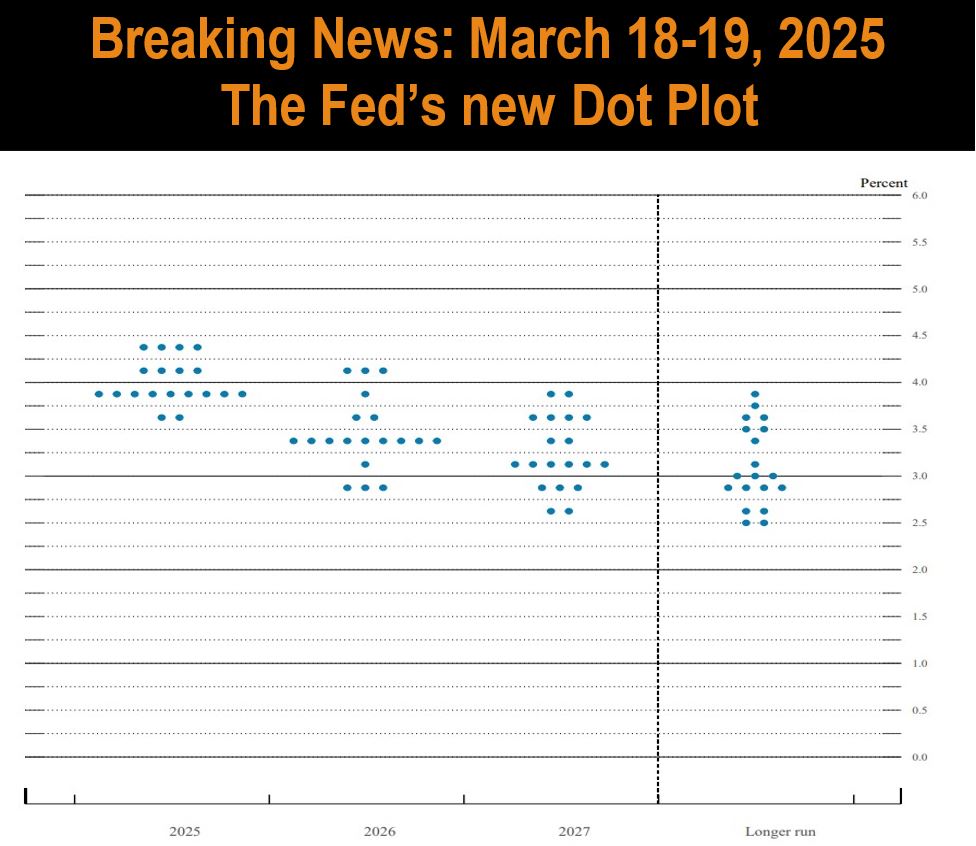

Summary of Economic Projections:

Interest rate forecasts:

Implementation note:

The Federal Reserve has made the following decisions to implement the monetary policy stance announced by the Federal Open Market Committee in its statement on March 19, 2025:

The Board of Governors of the Federal Reserve System voted unanimously to maintain the interest rate paid on reserve balances at 4.4%, effective March 20, 2025.

As part of its policy decision, the Federal Open Market Committee voted to direct the Open Market Desk at the Federal Reserve Bank of New York, until instructed otherwise, to execute transactions in the System Open Market Account in accordance with the following domestic policy directive:

"Effective March 20, 2025, the Federal Open Market Committee directs the Desk to:

“Undertake open market operations as necessary to maintain the federal funds rate in a target range of 4-1/4% to 4-1/2%.”

“Conduct standing overnight repurchase agreement operations with a minimum bid rate of 4.5% and with an aggregate operation limit of $500 billion.”

“Conduct standing overnight reverse repurchase agreement operations at an offering rate of 4.25% and with a per-counterparty limit of $160 billion per day.”

“Roll over at auction the amount of principal payments from the Federal Reserve's holdings of Treasury securities maturing in March that exceeds a cap of $25 billion per month.”

“Beginning on April 1, roll over at auction the amount of principal payments from the Federal Reserve's holdings of Treasury securities maturing in each calendar month that exceeds a cap of $5 billion per month.”

“Redeem Treasury coupon securities up to these monthly caps and Treasury bills to the extent that coupon principal payments are less than the monthly caps.”

“Reinvest the amount of principal payments from the Federal Reserve's holdings of agency debt and agency mortgage-backed securities (MBS) received in each calendar month that exceeds a cap of $35 billion per month into Treasury securities to roughly match the maturity composition of Treasury securities outstanding.”

“Allow modest deviations from stated amounts for reinvestments, if needed for operational reasons."

In a related action, the Board of Governors of the Federal Reserve System voted unanimously to approve the establishment of the primary credit rate at the existing level of 4.5%.

Note on operating policy:

Statement regarding reinvestment of principal payments from Treasury securities, agency debt and agency mortgage-backed securities.

At the meeting that concluded on March 19, 2025, the Federal Open Market Committee (FOMC) decided to slow the pace of decline in its securities holdings. Beginning in April, the Committee directed the Open Market Trading Desk at the Federal Reserve Bank of New York (the Desk) to reduce the monthly redemption cap on Treasury securities from $25 billion to $5 billion. The Committee will continue reducing holdings of agency debt and agency mortgage-backed securities (MBS) up to a monthly cap of $35 billion. Any principal payments received from agency debt and agency MBS holdings in excess of the $35 billion monthly cap will be reinvested into Treasury securities.

Consistent with current practice, the redemptions of Treasury securities each calendar month will include Treasury coupon securities and, to the extent that maturing coupon securities are less than the monthly cap, Treasury bills. The Desk will roll over at auction the amount of principal payments from System Open Market Account (SOMA) holdings of Treasury securities maturing during each calendar month that exceeds the cap amount for that month. The Desk will allocate Treasury coupon rollover amounts across the month’s coupon maturity dates in proportion to total SOMA coupon maturities on each date. The Desk will separately allocate bill rollover amounts across the month’s bill maturity dates in proportion to total SOMA bill maturities on each date. Rollovers will continue to be accomplished by placing non-competitive bids at Treasury auctions. The bids will be allocated across the securities being issued on each auction date in proportion to their announced offering amounts.

Should principal payments on SOMA holdings of agency debt and agency MBS exceed the $35 billion redemption cap, the Desk will announce the monthly amount of Treasury secondary market reinvestment purchases and a tentative schedule of purchase operations on or around the ninth business day of each month. Secondary market purchases will generally be conducted over the one-month period until the next announcement. Under this guidance, the Desk plans to distribute secondary market Treasury reinvestment purchases across nominal coupons, bills, Treasury Inflation-Protected Securities and Floating Rate Notes across a range of maturities to roughly match the maturity composition of outstanding securities.